Gaussian HMM of stock data¶

This script shows how to use Gaussian HMM on stock price data from

Yahoo! finance. For more information on how to visualize stock prices

with matplotlib, please refer to date_demo1.py of matplotlib.

from __future__ import print_function

import datetime

import numpy as np

from matplotlib import cm, pyplot as plt

from matplotlib.dates import YearLocator, MonthLocator

try:

from matplotlib.finance import quotes_historical_yahoo_ochl

except ImportError:

# For Matplotlib prior to 1.5.

from matplotlib.finance import (

quotes_historical_yahoo as quotes_historical_yahoo_ochl

)

from hmmlearn.hmm import GaussianHMM

print(__doc__)

Get quotes from Yahoo! finance

quotes = quotes_historical_yahoo_ochl(

"INTC", datetime.date(1995, 1, 1), datetime.date(2012, 1, 6))

# Unpack quotes

dates = np.array([q[0] for q in quotes], dtype=int)

close_v = np.array([q[2] for q in quotes])

volume = np.array([q[5] for q in quotes])[1:]

# Take diff of close value. Note that this makes

# ``len(diff) = len(close_t) - 1``, therefore, other quantities also

# need to be shifted by 1.

diff = np.diff(close_v)

dates = dates[1:]

close_v = close_v[1:]

# Pack diff and volume for training.

X = np.column_stack([diff, volume])

Run Gaussian HMM

print("fitting to HMM and decoding ...", end="")

# Make an HMM instance and execute fit

model = GaussianHMM(n_components=4, covariance_type="diag", n_iter=1000).fit(X)

# Predict the optimal sequence of internal hidden state

hidden_states = model.predict(X)

print("done")

Out:

fitting to HMM and decoding ...done

Print trained parameters and plot

print("Transition matrix")

print(model.transmat_)

print()

print("Means and vars of each hidden state")

for i in range(model.n_components):

print("{0}th hidden state".format(i))

print("mean = ", model.means_[i])

print("var = ", np.diag(model.covars_[i]))

print()

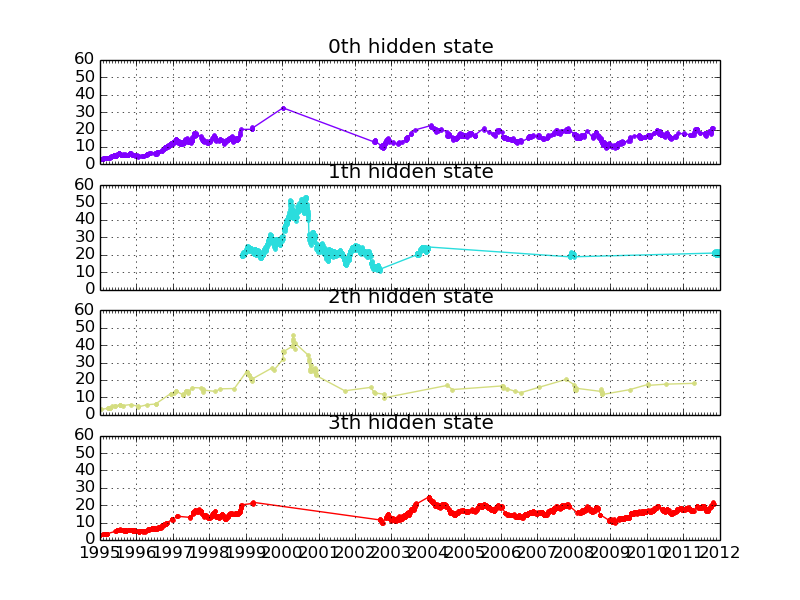

fig, axs = plt.subplots(model.n_components, sharex=True, sharey=True)

colours = cm.rainbow(np.linspace(0, 1, model.n_components))

for i, (ax, colour) in enumerate(zip(axs, colours)):

# Use fancy indexing to plot data in each state.

mask = hidden_states == i

ax.plot_date(dates[mask], close_v[mask], ".-", c=colour)

ax.set_title("{0}th hidden state".format(i))

# Format the ticks.

ax.xaxis.set_major_locator(YearLocator())

ax.xaxis.set_minor_locator(MonthLocator())

ax.grid(True)

plt.show()

Out:

Transition matrix

[[ 7.73505488e-01 1.21602143e-12 4.13525763e-02 1.85141936e-01]

[ 3.55338066e-15 9.79217702e-01 1.80611963e-02 2.72110180e-03]

[ 4.20116465e-01 1.18928463e-01 4.60955072e-01 1.91329669e-18]

[ 1.12652335e-01 3.25253603e-03 6.90794632e-04 8.83404334e-01]]

Means and vars of each hidden state

0th hidden state

mean = [ 2.19283455e-02 8.82098779e+07]

var = [ 1.26266869e-01 5.64899722e+14]

1th hidden state

mean = [ 2.40689227e-02 4.97390967e+07]

var = [ 7.42026137e-01 2.49469027e+14]

2th hidden state

mean = [ -3.64907452e-01 1.53097324e+08]

var = [ 2.72118688e+00 5.88892979e+15]

3th hidden state

mean = [ 7.93313395e-03 5.43199848e+07]

var = [ 5.34313422e-02 1.54645172e+14]

Total running time of the script: (0 minutes 2.219 seconds)

Download Python source code:

plot_hmm_stock_analysis.py

Download IPython notebook:

plot_hmm_stock_analysis.ipynb